Cristini Rosa Pinheiro, Orcid: https://orcid.org/0000-0002-7723-6252; Programa de Mestrado e Doutorado em Desenvolvimento Local - UNISUAM Centro Universitário Augusto Motta - RJ – Brasil. E-mail: crispdvsa@gmail.com

Patrícia Bilotta

, Orcid: https://orcid.org/0000-0002-2463-2331; Programa de pós-Graduação em Desenvolvimento Local - UNISUAM - Centro universitário Augusto Motta - Rio de Janeiro - RJ – Brasil. E-mail: pb.bilotta@gmail.com

Abstract

In recent decades, the production and consumption patterns that characterize the population in general have contributed to the worsening of the socioenvironmental crisis, which is due to the lack of commitment to the principle of the sustainability, especially among the business sector. These circumstances have given rise to the concept of the “B Corporation”, which brings together organizations that seek solutions to socioenvironmental problems in conjunction with their normal operations as private entities. The purpose of this article is to identify opportunities and challenges in socio-environmental practices and corporate governance from the perspective of “B Corporation” certification. The methodology is based on: (i) bibliographic survey; (ii) documentary research; and (iii) development of a SWOT matrix. The results recognize several Brazilian companies (such as Natura and Granato) as belonging to this segment. Although this is a growing movement that can create new market opportunities and change the behavior of those who consume these products, many companies still have doubts regarding regulatory aspects of the market, making it difficult for a greater number of organizations to enter the segment.

Keywords: Corporate sustainability. Social and environmental responsibility. B Corporation Movement. Low carbon economy.

Resumo

Nas últimas décadas, os padrões de produção e consumo da população têm contribuído para o agravamento da crise socioambiental, devido ao não comprometimento com a sustentabilidade, principalmente o setor empresarial. Assim, emerge o conceito de “Empresa B”, que reúne organizações que buscam resolver problemas socioambientais paralelamente ao desenvolvimento de suas atividades como entidade privada. O objetivo deste artigo é identificar oportunidades e desafios nas práticas socioambientais e de governança corporativa sob a perspectiva da certificação “Empresa B”. A metodologia se apoia em: (i) levantamento bibliográfico; (ii) investigação documental; (iii) construção da matriz SWOT. Como resultado: várias empresas brasileiras são reconhecidas nesse segmento (por exemplo, Natura, Granato). Esse movimento está crescente e pode criar oportunidades de mercado e mudança no comportamento dos consumidores desses produtos, mas ainda existem muitas dúvidas das empresas em relação a aspectos regulatórias de mercado que dificultam o ingresso de um maior número de organizações nesse segmento.

Palavras-chave: Sustentabilidade corporativa. Responsabilidade socioambiental. Movimento B. Economia de baixo carbono.

In recent years, the term Environment, Social, and Governance (ESG), also known as corporate sustainability practices, has been widely used in the corporate context. The concept emerged in the 2005 report “Who Cares Wins”, published under an initiative led by the United Nations, which included 20 financial institutions from 9 countries, including Brazil (ESGBRASIL, 2021). Guidelines and recommendations were created that covered environmental, social and governance issues in asset management, securities brokerage services and related topics, based on the understanding that these elements have the potential to generate more sustainable markets and deliver superior economic results (CANABARRO et al., 2021). Since then, companies have made efforts to present campaigns and projects aligned with socio-environmental responsibility actions for the purpose of demonstrating that their corporate activities have a positive impact and can meet the sustainability demands of their customers (VILELA, 2021).

A Brazilian study involving companies in the industrial segment, revealed that although approximately 80% of the companies interviewed in the survey recognized the importance of including topics related to the environment in their business strategies, only 15% related their corporate goals to the 17 Sustainable Development Goals (SDG) of the United Nations 2030 Agenda (RICHTER et al., 2017), which seeks to ensure the quality of human life and environmental health, including the maintenance of the climate system (UN, 2015). It is also seeking to identify and strengthen the commitment to adequate environmental and social practices among stakeholders and identify relevant issues in their business (VILELA, 2021; RICHTER et al., 2017).

Sustainability practices (ESG) are much more than a simple positive bond between the company and its customers and stakeholders; their goal is to create an awareness in the company of its responsibility as an active agent of transformation in society. Companies that are not currently aligned with sustainability principles face difficulties from increasing restrictions by the investor market (VILELA, 2021). Since ESG practices tend to increase returns on investments, progressive investors seek portfolios on the ESG-efficient frontier (PEDERSEN; FITZGIBBONS; POMORSKY, 2021).

A corporation that adopts sustainability practices as an active principle triggers a series of positive impacts (environmental quality, social responsibility, benefits for its employees, impact on society and on the company's financial strategy), since ESG actions represent a real paradigm shift in the relationships traditionally established between companies and their investors (VILELA, 2021). As a result, companies over the last few years have been seeking to improve the reporting of their ESG practices; however, one of the most important challenges in this respect lies in the lack of a standardized and widely accepted metric.

The application of ESG practices guides the industry management models and sustainable production; this is based on the reduction of environmental damage, humanization, diversity, social inclusion, and the maximization of economic and financial return, to guarantee the company's operation. Examples of the type of actions an industry must implement include the conscientious acquisition of raw materials and reverse logistics for non-recyclable packaging (YOSHIDA et al., 2021).

From the standpoint of corporate sustainability practices, it is essential that the industrial sector transition to a low-carbon economy to direct investments toward energy efficiency strategies and replace fossil fuels with renewable alternatives (THEIS and SCHREIBER, 2021). A survey conducted in the United States by the Climate Accountability Institute revealed that 20 oil companies are responsible for more than 1/3 of all global greenhouse gas (GHG) emissions (RAMOS et al., 2023). Thus, companies that support such a change will benefit from new business opportunities, and their brand will stand out positively among the most demanding consumers (HEEDE, 2021).

One such initiative for the encouragement of a low-carbon economy in the corporate environment is Science Based Targets, an organization created as a partnership among the World Wild Fund for Nature (WWF), the United Nations (UN) Global Compact, the Carbon Disclosure Project (CDP Worldwide) and the World Resources Institute (WRI) for the purpose of helping the business sector meet targets for GHG emission reductions and supporting strategies for carbon neutrality in the production process (GLOBAL COMPACT, 2023; ESGBRASIL, 2021).

The progressive substitution of the classic production model with a more sustainable model is the result of the growing demand for socio-environmentally friendly (eco-friendly) products, whether due to demands from more conscientious consumers and investors or to legal restrictions; however, this transition needs appropriate instrumentation to support corporate decisions regarding updates in technology and strategy. Thus, the objective of this article is to identify opportunities and challenges in socio-environmental and corporate governance practices from the standpoint of “B Corporation” certification.

Sustainability management systems are a reaction to organization and the consumer desires for acceptable products, generated by companies that assume socio-environmental responsibility. Business organizations, in turn, seek to balance their activities in the economic, social, environmental, spatial, or cultural spheres. As a result, organizations are increasingly looking for management systems that aim to balance these demands (NORTHOUSE, 2004).

Management structures are valuable operating systems that support organizational wisdom and continuous improvement. Tools for improving socio-environmental awareness include Ritmo Natural, the Announcement of Human Rights, Agenda 21, the Earth Charter, and the Millennium Goals. Management tools include ISO, EMAS, and ABNT/NBR 16000 series (MATTEN and MOON, 2008), which establish important control indicators for measuring the organizational performance in a broader context. Assessments or audits usually request code standards based on specific metrics for each question (SILVA, 2021).

Sustainability reports, which provide information about a company's socio-environmental achievements, present results to the external public and help to improve internal process management. Internal recommendations incorporate the results into management structures to improve performance regarding social, economic, and environmental benchmarks (GUTIÉRREZ et al., 2016). Corporate sustainability seeks a balance between social, environmental, and economic interests. These topics are currently the center of much discussion and can have a tremendous impact on company reputation and commercial brands (MELO, 2005). However, many organizations face difficulties in hiring consultants or training personnel to meet the demands of society regarding the minimum requirements of corporate governance, social responsibility, and sustainability. It is therefore necessary that adequate instruments be developed to deal with these issues in a simplified and gradual manner (WOOT, 2011).

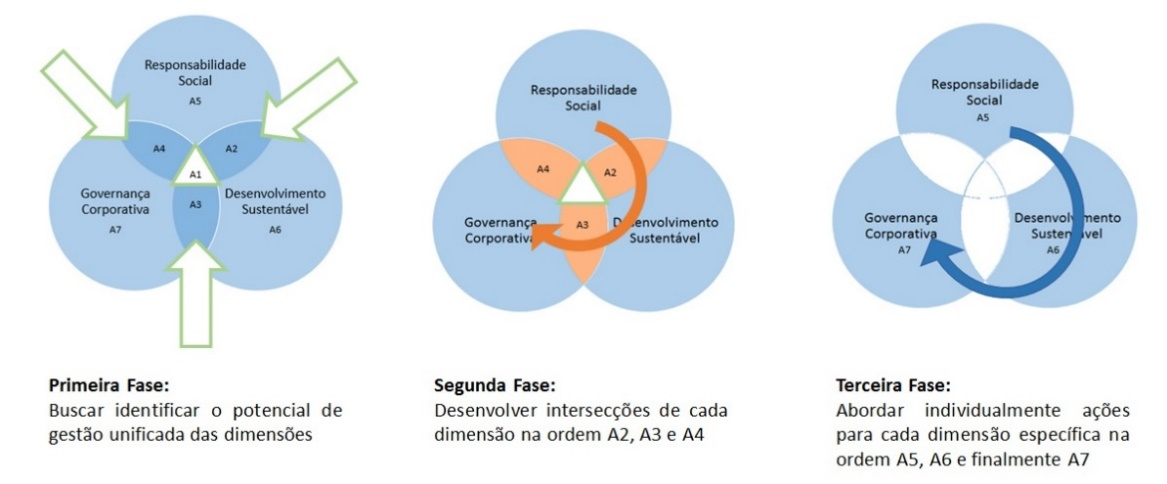

The concept of globally sustainable corporate responsibility (RCGS) was developed by the World Economic Forum. RCGS is a global sustainability assessment and measurement protocol (CLARO, 2008) that aims to integrate different approaches to sustainable development (SD), social responsibility (SR) and corporate governance (CG), with the aim of optimizing positive impacts of companies on society in a way that is more “efficient and effective” in the implementation of the various criteria (CARROL and SHABANA, 2010; MACHADO, 2006) (Figure 1). The three dimensions addressed in the RCGS methodology (DS, RS, GC) share the objective of promoting business management based on ethics, transparency, and actions that are socially responsible and environmentally sustainable (ZELDIN et al., 2000).

Figure 1 - Interrelationship of the theoretical bases of social responsibility (SR), corporate governance (GC) and sustainable development (SD).

Source: Machado (2006).

Table: Social Responsibility, Corporate Governance, Sustainable development

First Stage: Search for and identify potential for unified management among the dimensions

Second Stage: Develop intersections of each pair of dimensions using the sequence A2, A3, and A4

Third Stage: Consider actions for each specific dimension individually, using the sequence A5, A6, and A7

Since the end of the last century, organizations have been seeking solutions such as assessment tools and sustainability indexes to mitigate the impact of their activities on the environment. One such index, the Corporate Sustainability Index (ISE), developed by the Brazilian Stock Exchange (B3) and headquartered in the city of São Paulo, was the first of its kind in Latin America. Its objective was to create an investment environment that is adaptable to the demands of sustainable development, as well as to encourage ethical responsibility among organizations (NASCIMENTO et al., 2020).

The socio-environmental externalities generated by an organization's activities soon became an active part of business management and economic sustainability, linked to the organization’s capacity for innovation regarding these new demands. Added to this is the impact of the COVID-19 pandemic, which brought to the fore the need for a resilient supply chain, reverse logistics and the circular economy (STREIT et al., 2022).

On the other hand, the Instrument for the Assessment of Sustainability and Strategic Planning (LASPE) exists to help companies understand the degree to which sustainability has been incorporated into their planned development practices (LOUETTE, 2007). The recommendations of the Brazilian Securities and Exchange Commission (CVM) regarding corporate governance seek to provide guidance on issues that have the potential to significantly affect relationships among administrators, directors, independent auditors, and both majority and minority shareholders (HENDERSON, 2003). The best corporate governance practices are designed to help create a more effective governance system within an organization (ZELDIN et al., 2000). Priority has been given to those principles of international guidelines and standards that have achieved widespread acceptance and visibility and have been applied in most countries for the purpose of guiding, encouraging, and promoting sustainable development, social responsibility, and the adoption of a good corporate governance (LOUETTE, 2007).

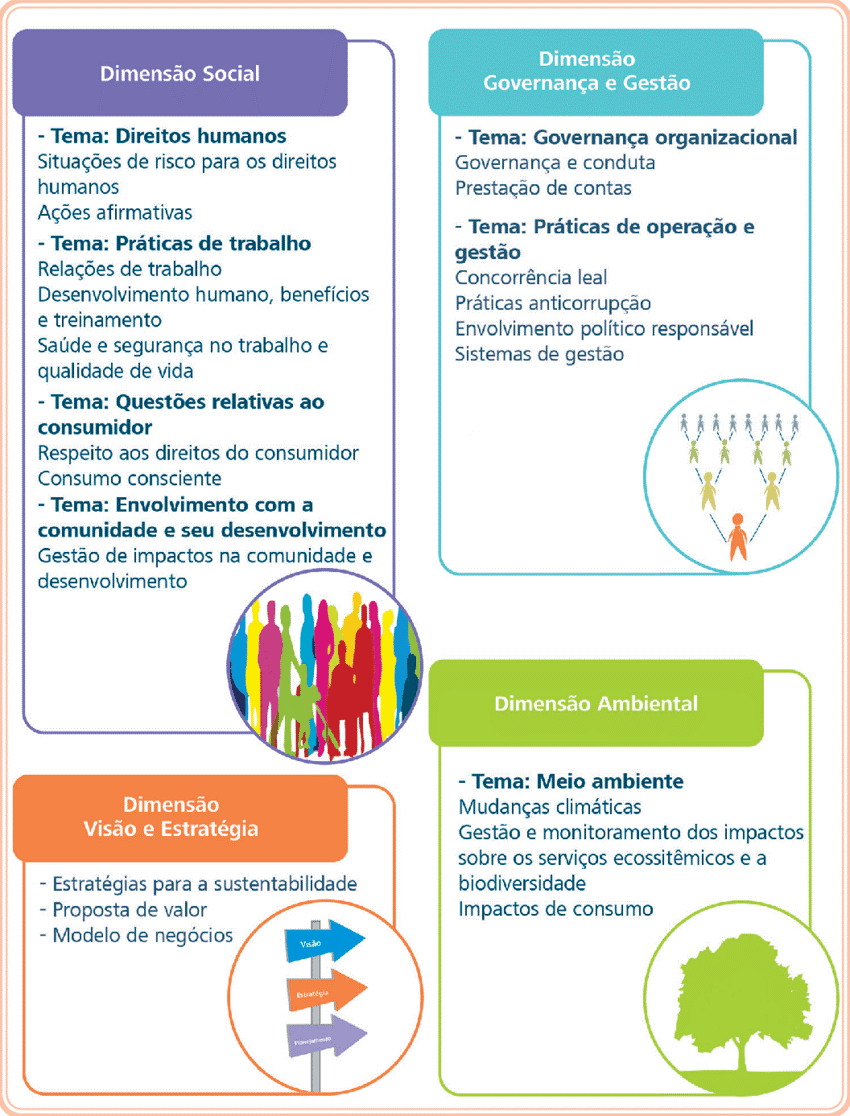

The Global Reporting Initiative (GRI) indicators focus on universally applicable guidelines for providing information regarding the sustainability of a given organization. The indicators are grouped into three categories: human rights, labor relations, and the environment (Figure 2). The GRI provides a series of qualitative and quantitative criteria for reporting corporate economic, environmental, and social performance (COMINI et al., 2014).

Figure 2 - Dimensions of the GRI indicators.

Source: Rodrigues (2016).

Social dimension Governance and Management Dimension

Theme: Human rights Theme: Organizational governance

Situations that represent a risk for human rights Governance and conduct

Affirmative action Accountability

Theme: Work Practices Theme: Operations and management practices

Work relations Fair competition

Human development, benefits, and training Anti-corruption practices

Health and safety at work and quality of life Responsible political involvement

Management systems

Theme: Issues related to the consumer

Respecting consumer rights

Conscientious consumption

Theme: Involvement with the community and its development

Management of impacts on the community and its development

Vision and Strategy Dimension Environmental Dimension]

Sustainability strategies Climate change

Value proposition Management and monitoring of impact on ecosystem

Business model services and biodiversity

Impacts of consumption

The methodology used was that of exploratory and analytical research based on qualitative data, which in turn is based on: (i) a bibliographical survey of corporate sustainability management instruments, through the content analysis of scientific articles identified in the Portal de Periódicos da Capes; (ii) documentary investigation of the criteria established in “B Corporation” certification, through content analysis available on the B Corporation platform (www.bcorporation.net/en-us/programs-and-tools/b-impact-assessment/); (iii) the development of a SWOT matrix using the main impacts of “B Corporation” certification (opportunities and challenges), based on the analysis of the results of the previous stages.

The SWOT matrix was chosen as a tool for analyzing aspects regarding the impact on the strategic planning of companies (opportunities and challenges), as its robustness and accessibility (NAMUGENYIA et al., 2019).

Development based on sustainability affects planning in trade, consumption, and production, not only from the perspective of economic relations, but also regarding behavior, habits, and values, aspects which are conditioned by the power relations in which individuals, groups and social classes engage in a specific geographical area (THEIS, 2008). Therefore, recent years have seen an increase in demand for environmental control, conservation, and improvement policies in companies in search of new governance models aligned with sustainability (BARRETO and MOREIRA, 2015).

The “B Corporation” segment represents businesses that meet the highest standards of socio-environmental performance, transparency criteria and legal responsibility by balancing profit and purpose and consider the impact of their decisions on their workers, customers, suppliers, communities, and environments (DA SILVA et al., 2022; BARRETO and MOREIRA, 2015). This category comprises companies that seek to be better for the world and not just be the best in the world (RODRIGUES, 2016).

The movement emerged in 2006 as an effort to build a more inclusive and sustainable economy (DIEZ-BUSTO et al., 2021) (Figure 3). The “B Corporation” segment is not only a means of recognizing the qualities of a product or service, but also a tool for monitoring and measuring factors that reveal the economic performance of the business, considering its social and environmental performance as it conducts its operations (CARVALHO FILHO et al., 2018). Organizations that fall under the “B corporation” category are committed to the purpose of continuous improvement in the eyes of the community and adopt this criterion at the heart of their business model (RODRIGUES, 2016).

Figure 3 – Evaluation dimensions of the “B Corporation” system.

Source: Sistema B (2021).

Certification requirements begin with the application of the B Impact Assessment (BIA), an instrument that assesses the relationship between a company and its employees, customers, group, and environment (DIEZ-BUSTO et al., 2021). This data is analyzed to evaluate the credibility of the information and notify investors to make an impact. The BIA is a free tool for assessing the socio-environmental impact of a company based on information regarding its operations and behavior over the previous last fiscal year, therefore, businesses must have at least 12 months of operation, otherwise it must opt for the Pending B Corp Seal (RODRIGUES, 2016). The following dimensions (also called areas of impact) are considered: corporate governance, employees, community, environment, and customers. The score ranges from 80 (minimum) to 200 (maximum) (DIEZ-BUSTO et al., 2021).

The following are several of the most important aspects of the BIA tool: data collection in structured processes/systems; identification of interruptions in tolerance periods; signaling of the effects caused by the interruption; identification of predilection criteria (cost x impact); persons responsible and their substitutes, including their respective contacts; designation of the RTO (Recovery Time Objective), defined as the period of time within which processes must be restored after an incident occurs in order to avoid major consequences, such as loss of business continuity; RPO (Recovery Point Objective) designation, defined by the maximum time that data can be lost or remain inaccessible due to an accident (DA SILVA et al., 2022; DIEZ-BUSTO et al., 2021; SYSTEM B, 2021).

Therefore, impact analysis is not an end. It is the starting point for using information and building other types of knowledge (such as risk analysis) or even for creating an action plan for the more alarming scenarios described in the documentation (RODRIGUES, 2016).

There are currently more than 3,500 organizations classified as “B Corporation” in 70 countries, and more than 120,000 companies that use the BIA tool to analyze their impact. The BIA model allows organizations to disseminate data, raise awareness and take concrete action to minimize their negative impacts (whether they be economic, social, or environmental), offering a robust and holistic approach for monitoring and assessment of social and environmental impacts caused by company activities (RODRIGUES, 2016).

BIA is an online digital platform that is open, confidential, and easy-to-use. It has a standardized structure, separated into five “areas of influence” that evaluate the following aspects: Governance; Workers; Community; Environment; Customers (COMINI et al., 2014). Each area is structured according to “impact themes” that report the specific impact dimensions related to the theme in question. Weighted questions provide a means of measuring the company's positive impact regarding its policies, guidelines, and company results. Impact topics may also include scoring questions. This provides additional context and helps to improve self-report accuracy (RODRIGUES, 2016).

Although the B System helps with all performance in the development of certification for companies, certification is established and provided only by the B-Lab by means of the B Impact Assessment (BIA) questionnaire and both on-site and documental analysis. The BIA undergoes assessment every three years, and certified companies must be recertified every two years (COMINI et al., 2014). In this regard, it must be emphasized that the achieving certification is one of the ways to identify and point out many distinctive aspects of companies. Moreover, since self-declaration methods always tend to generate a lack of confidence on the part of stakeholders regarding the sustainability standards of companies, third parties can provide more reliable data due to their detachment from what is verified (CAMPOS et al., 2013).

Certification grants companies the right to use the BCorp seal (B-LAB, 2018). Companies that use the free BIA tool must achieve at least 80 points from a total of 200. BIA questions and scores are developed according to the individual company’s place of activity, the market in which it operates, and the number of employees (DIEZ -BUSTO et al., 2021; SYSTEM B, 2021) (Table 1).

Table 1 - Overview of the content covered by the BIA.

|

IMPACT AREAS |

DIMENSIONS |

SDG RELATED |

OVERVIEW |

|

Governance |

Mission and engagement, ethics and transparency, governance metrics, protection of the company's mission |

“Peace, justice and effective institutions” (16) |

Analyzes the company's vision, ethics, responsibility, and transparency |

|

Employees |

Metrics involving employee financial security, safety and well-being, professional development, engagement, and satisfaction |

“Decent work and economic growth” (8) |

Analyzes the company's contribution to the well-being of employees, aspects related to compensation and benefits, training, health, safety, and flexibility |

|

Community |

Diversity, equity, inclusion, economic impact, civic engagement, giving, supply chain management |

“Responsible consumption and production” (12), “Action against global climate change” (13), “Life in the water” (14), “Terrestrial life” (15) |

Analyzes the company's relationship/impact on the community, company diversity, job creation, relationship with suppliers, charitable donations, volunteer work, local involvement |

|

Environment |

Environmental management, air and climate management, water, land and life management

|

“Drinking water and sanitation” (6), “Life in the water” (14), “Terrestrial life” (15) |

Evaluates the company's environmental management, company facilities, use of resources, emissions, supply chain and distribution channels |

|

Clients |

Client management |

“Partnerships and means of implementation” (17) |

Evaluates the impact of the company on customer relations, with an emphasis on offering products/ services for the public good |

Source: The authors.

The prospect of attracting customers is an adequate justification for adhering to seals and certifications, which serve as a way in which the company may distinguish itself, thus helping consumers to purchase products and services with greater socio-environmental commitment (CAMPOS et al., 2013). Another key point made by the author is that such certifications and seals are also a means for bringing the organization’s stance in line with that of its stakeholders, while at the same time building a positive image. Even before the B System was launched in Brazil, some Brazilian companies had already applied the BIA tool for internal assessment and for the purpose of achieving certification. After its implementation in Brazil, the number of companies adhering to the tool and seeking certification has increased every year (SISTEMA B, 2021).

Some examples of certified B Corps in Brazil are: 99jobs.com; Alaya, AMATA, AMMA Chocolate, Aoka, Araruna Filmes, 4You2, Asta, Avante, Baluarte Cultura, Broota, Caos Design, Carioteca, Casa do Futuro, CAUSE, CBPAK, ComBio Energia, Courrieros, Daterra, Dinamo, EcoSocial, eCycle, Eureciclo , Fazenda de Toca, Flavia Aranha, Fomenta, Granato, Grupo Gaia, Geekie, Indi.us, InsectaShoes, I already understood, Juçaí, Mãe Terra, Maria Farinha Filmes, MateriaBrasil, Mayra Abucham, MOV, Natura (SISTEMA B, 2021).

As of December 2018, there was a total of 131 certified companies in Brazil, and 21 organizations with pending “B Corporation” certification. The responsible of the B System for certification is based on several factors. For example, the administration website lists eight aids: protection of the mission, access to investors, global movement, continuous improvement, talent acquisition, access to customers, positioning (positive exposure) and economy (SYSTEM B, 2021). This catalog is even greater in the B Corp Manual for being involved in a society of leaders with distributed values, conquering talent and attracting employees, growing credibility and gaining strength, creating press coverage, benchmarking and improving development, attracting investors, preserving the mission of a company over a long period of time, creating a set of voices, saving money and commanding a global movement (DIEZ-BUSTO et al., 2021; COMINI et al., 2014).

The consequences of business, product and service impact assessments also cover critical links in an organization's supply chain and can be used as input to define business strategy, identify, and manage future risks and opportunities, prioritize investments, etc. (BUENO and BRIGHT, 2020). Some examples of how impact evaluations may be used strategically are:

Therefore, it is essential that companies not only pursue purely financial results related to the generation or destruction of value, but also analyze the impact of their operations, including their value chain, on socio-environmental aspects (BUENO and BRIGHT, 2020).

In managing the impact on business, it is important that companies develop assessment tools that estimate, recognize, measure, and reveal both beneficial and negative impacts. However, for this assessment to be effective, companies must consider a broad spectrum of stakeholders that goes beyond customers, suppliers, and investors. It is therefore necessary to understand how social externalities (e.g., accidents and fatalities, employee satisfaction, investment in inclusive business) and environmental externalities (e.g., air and water pollution and waste production) affect indicators such as employee motivation or availability of natural resources (BUENO and BRIGHT, 2020).

Despite its importance, however, only 31% of the companies that prepare the impact study carry out this activity correctly, according to SAM's 2020 Sustainability Yearbook. The main problem identified is that these assessments fail to focus on and complement aspects that have not yet been observed in the financial reports of the organizations (S&P GLOBAL, 2020). Therefore, it is necessary to go beyond the impacts already included in the famous Value-Added Declaration (DVA) and identify company impacts (both positive and negative) that have not yet been integrated into its financial statements (SOUZA and FARIA, 2018).

The results of the SAM Sustainability Yearbook show a strong emphasis on identifying the environmental impact, since only 38% of the instances identified were social issues. However, it should be noted that environmental and social impacts are often inseparable and should not be considered in isolation (S&P GLOBAL, 2020).

The industries with the greatest impact assessment considering several aspects that have not yet been classified in company financial statements are the following sectors: energy, information technology materials; products and services. More than 20% of companies in these sectors say they have performed this type of assessment. It is interesting to note that the best placed sectors are those already known for their relevant impact on environmental and social issues (BUENO and BRIGHT, 2020). At another level of analysis, it is known that most company impacts are related not only to their operations, but also to their supply chains, which can be quite complex and incorporate various sectors and regions. Each link in the chain has a set of external factors that need to be mapped (YOSHIDA et al., 2023).

Overall, only 43% of companies have externalities throughout the lifecycle of their products and services. These values vary according to the characteristics of each sector examined. For example, 61% of financial sector companies generally underperform. There are external factors indirectly related to the services of companies from this sector (such as the impact of the operations in which they invest). On the other hand, 80% of energy companies report external factors related to their activities (SAMUELSEN et al., 2020). There are several ways to measure the cost and/or benefit of a given impact, and these can help in the strategic decision-making process. A quantitative approach can show the magnitude of a company's impact, both financially and non-monetarily.

The B Corp movement seeks to provide a solution to the growing realization that the corporate embrace of “shareholder primacy” is the root cause of many of the fundamental problems facing the world. Politicians as diverse as Senators Marco Rubio and Elizabeth Warren have condemned the shareholder-first philosophy, saying it has been a disaster for the US economy (YUNUS et al., 2014).

The B Corp model provides tools, methods, and legal frameworks for companies to align their operations with long-term values. It also helps build trust and brand equity among the public. Until recently, B Lab focused on small and medium-sized companies such as Kickstarter, Allbirds, Casper and Bombas (MUSIAL et al., 2022). Figure 4 presents the SWOT matrix based on the perception of the aspects of opportunities and threats (external to the company), and strength and weakness (internal to the company).

Figure 4 - SWOT matrix.

|

Internal |

STRENGTH: Planning and management: understand the evolution of management systems and norms and search for the models that are best suited for each organization. Conduct an in-perspective discussion of the development of norms, analyze and reflect on new perspectives for certification whose goal is to promote practices that are more responsible, ethical, and sustainable. |

WEAKNESS: Achieve a balance between financial priorities and social and environmental aspects: a carefully orchestrated environmental strategy is vital for long-term success. It is essential that the planning developed be in line with and integrated with strategic initiatives that are already in place in the company and coordinated with an approach that considers the risks and benefits involved. |

|

External |

OPPORTUNITY: The implementation of social responsibility (ESG) in the culture of the organizations: Understand how management systems approach the practice of social responsibility and engagement with stakeholders and define the role of leadership and management in the organizational culture. It is essential to reflect on the importance of management practices, processes, and systems, while also recognizing the importance of values, the role of the behavior of the leaders in organizational learning, and the place of communication that is strategic, contemporary, and legitimate. |

THREAT: Understanding motivations and context: the alignment of diverse contemporary issues within the organization, such as the impact of the pandemic, the shock on the corporate world, the origins of and current challenges involving sustainability, and the importance that is being given to the agenda. Incorporate the main sustainability concepts, sustainable development, socioenvironmental responsibility, and its roots in ethical values. |

Source: The authors.

The question is whether the certification system can be adapted for certification of large multinational companies. Some supporters believe that the integrity of the movement would be diluted if large companies were to join. In the wake of the pandemic, it is necessary to build a more sustainable and resilient economic model. Large companies and publicly traded multinationals must adopt rigorous methods (MUSIAL et al., 2022).

The above example also shows the relevance of contextualizing reported impacts. The company's external reports alone may not reflect the impact it has experienced. The excessive water consumption that occurred in the city of São Paulo in 2014, in conjunction with the severe water shortage, can hardly be compared to the similar level of water consumption in 2020 (BUENO and BRIGHT, 2020).

This article provides an analysis of the opportunities and challenges facing socio-environmental and corporate governance practices from the perspective of an important analysis tool: the “B Corporation” segment.

It was found that the business strategies implemented by the “B Corporation” segment: I) are strongly linked to their environment and interest groups; II) are based on tacit scientific and technological knowledge that represents a key factor for the development of environmental, technological, organizational, product and process innovations; III) are formulated in favor of the most vulnerable classes in the communities in which they operate (for example, the inclusion of women, small local producers, and marginalized classes in the working world); IV) allow for the creation of strong ties with other companies or local actors by means of alliances, associations, cooperatives for the exchange of raw materials, knowledge, services or collective benefits; V) promote the diversification of the production structure of the locations in which they operate; VI) contribute to environmental sustainability, incorporating practices that mitigate negative impacts on the environment and conserve both natural resources and biological diversity; VII) preserve the natural heritage, traditions, and culture of individual communities; VIII) reduce social inequalities in communities, promoting training plans and improving employment, housing, and consumption habits. This is based on the characteristics and nature of the industry in which organizations in the “B Corp” segment operate.

Therefore, it may be concluded that within the framework of the demands of sustainable development and in the context of the knowledge society, the long-term ability of organizations to maintain their operations lies in their ability to develop management models that incorporate knowledge management based on stakeholder interests in three areas of sustainability: resources and environmental impact, the economic environment, and the social or human sphere. Such models allow companies to create innovations that add value and improve their competitiveness, contributing to the economic, social, and environmental development of individual communities.

It is suggested that future research focus on public policies aimed at tax incentives, differentiated lines of credit, and legal mechanisms for assessing socio-environmental performance (among other instruments) for the purpose of encouraging sustainable operations in companies and developing other management tools whose results may be compared with those of the SWOT matrix.

BARKI, E. Negócios de impacto: tendência ou modismo? Sociedade e Gestão, v. 14 (1), p. 14-17, 2015.

BARRETO, T. S.; MOREIRA, R. N. Impacto Ambiental provocado pela destinação incorreta de Pneus. Revista Eniac Pesquisa, v. 4 (2), 162-175, 2015.

BUENO, N.; BRIGHT, C. Implementing human rights due diligence through corporate civil liability. International & Comparative Law Quarterly, v. 69(4), p. 789-818, 2020.

CAMPOS, L.M.S.; SEHNEM, S.; OLIVEIRA, M.A.S.; ROSSETTO, A.M.; COELHO, A.L.A.L.; DALFOVO, M.S. Relatório de sustentabilidade: perfil das organizações brasileiras e estrangeiras segundo o padrão da Global Reporting Initiative. Gestão & Produção, v. 20, p. 913-926, 2013.

CANABARRO, R.S.; ALMEIDA, D.M.; IBDAIWI, T.K.R.; GOULART, S.O. Impacto Socioambiental: a contribuição das malharias de Santa Maria/RS. Anais do IV Simpósio Sul-Mato-Grossense de Administração, v. 4 (4), p. 518-533, 2021.

CARROL, A.B.; SHABANA, K. M. The business case for corporate social responsibility: A review of concepts, research, and practice. International journal of management reviews, v. 12 (1), p. 85-105, 2010.

CARVALHO FILHO, M.; PIMENTEL, S.M.; BERTINO, R.M.J.; OLIVEIRA, A.R.L. Índice de sustentabilidade empresarial: Uma análise acerca da evidenciação do passivo ambiental. Revista Ambiente Contábil, v. 10 (1), p. 104-120, 2018.

CLARO, P.B.O. Entendendo o conceito de sustentabilidade nas organizações. Revista de Administração-RAUSP, v. 43 (4), p. 289-300, 2008.

COMINI, G. M.; FIDELHOLC, M.; RODRIGUES, J. Empresas B: princípios e desafios do movimento B Corp. In: XVII SEMINÁRIOS EM ADMINISTRAÇÃO, SemeAd – PPGA FEAUSP, São Paulo, 2014.

DA SILVA, H.T.; DOS SANTOS, M.J.; KLEINOWISKI, H.L. Sustentabilidade em pequenos negócios: uma abordagem baseada nos padrões da Empresa B. Revista Conectus: Tecnologia, Gestão e Conhecimento, v. 2 (1), 2022.

DIEZ-BUSTO, E.; SANCHEZ-RUIZ, L.; FERNANDEZ-LAVIADA, A. The B Corp movement: a systematic literature review. Sustentability, v. 13 (5), p. 2508, 2021.

ESGBRASIL. Rede Brasil do Pacto Global. Ed. São Paulo, 2021. Available in: www.gruponewspace.com.br

GUTIÉRREZ, R.; MÁRQUEZ, P.; REFICCO, E. Configuration and Development of Alliance Portfolios: A Comparison of Same-Sector and Cross-Sector Partnerships. Journal of Business Ethics, v. 135, p. 55-69, 2016.

HEEDE, P. Effective and sustainable use of municipal solid waste incineration bottom ash in concrete regarding strength and durability. Resources, Conservation and Recycling, v. 167, p. 105356, 2021.

HENDERSON, J.V. Urbanization and economic development. Annals of Economics and Finance, v. 4 (2), p. 275-342, 2003.

JOSEPH, N.; KUMAR, A.; MAJGI, S.M.; KUMAR, G.S.; PRAHALAD, R.B.Y. Usage of Plastic Bags and Health Hazards: A Study to Assess Awareness Level and Perception about Legislation among a Small Population of Mangalore City. Journal of Clinical and Diagnostic Research, v. 10, LM01-LM04, 2016.

LOUETTE, A. Gestão do conhecimento: compêndio para a sustentabilidade, ferramentas de gestão de responsabilidade socioambiental. Antakarana Cultura Arte Ciência: São Paulo, ed. 1, 2007, 186 p.

MACHADO, D.G. Análise das relações entre a gestão de custos e a gestão do preço de venda: um estudo das práticas adotadas por empresas industriais conserveiras estabelecidas no RS. Revista Universo Contábil, v. 2 (1), p. 42-60, 2006.

MATTEN, D.; MOON, J. RSC “Implicit and explicit CSR: a conceptual framework for a comparative understanding of corporate social responsability. Academy of Management Review, v. 33 (2), p. 404-424, 2008.

MELO, R. D. S. O turismo em ambientes recifais: em busca da transição para a sustentabilidade. Caderno virtual de turismo, v. 5 (4), p. 34-42, 2005.

MUSIAL, W.; SPITSEN, P.; DUFFY, P.; BEITER, P.; MARQUIS, M.; HAMMOND, R.; SHIELDS, M. Offshore wind market report. Technical Report, 2022. Available in: www.osti.gov/biblio/1883382

NAMUGENYIA, C.; NIMMAGADDAB, S. L.; REINERSC, T. Design of a SWOT Analysis Model and its Evaluation in Diverse Digital Business Ecosystem Contexts. Procedia Computer Science, v. 159, p. 1145–1154, 2019.

NASCIMENTO, I.C.S.; SANTOS, A.R.S.; PESSOA, A.F.P. GUIMARÃES, D.B.; REBOUÇAS, S.M.D.P. Internacionalização e sustentabilidade empresarial no Brasil. Revista Eletrônica de Negócios Internacionais, v. 15 (3), p. 63-79, 2020.

NORTHOUSE, L. Coping strategies and quality of life in women with advanced breast cancer and their family caregivers. Psychology & Health, v. 19 (2), p. 139-155, 2004.

PACTO GLOBAL, Rede Brasil. ESG: Entenda o significado da sigla ESG (Ambiental, Social e Governança) e saiba como inserir esses princípios no dia a dia de sua empresa, 2023. Available in: www.pactoglobal.org.br/pg/esg

PEDERSEN, L.H.; FITZGIBBONS, S.; POMORSKI, L. Responsible investing: The ESG-efficient frontier. Journal of Financial Economics, v. 142 (2), p. 572-597, 2021.

RAMOS, J.M.; CORREA, E.C.D.; AMORIM, I.S. O desenvolvimento sustentável e a cidadania global: o papel das bibliotecas para o alcance dos objetivos e metas da agenda 2030 da ONU. Ciência da Informação em Revista, v. 10 (1/3), p. 1-16, 2023.

RICHTER, C.; KRAUS, S.; BREM, A.; DURST, S.; GISELBRECHT, C. Digital entrepreneurship: innovative business models for the sharing economy. Creativity and Innovation Management, v. 26 (3), p. 300-310, 2017.

RODRIGUES, J. O movimento B Corp: significados, potencialidades e desafios. Dissertação (Mestrado em administração) – USP, São Paulo, 2016. Available in: https://www.teses.usp.br/teses/disponiveis/12/12139/tde-19122016-152403/en.php

SAMUELSEN S.; SHAFFER B.; GRIGG J.; LANE B.; REED J. Performance of a hydrogen refueling station in the early years of commercial fuel cell vehicle deployment. Internacional Journal of Hydrogen Energy, v. 45, p. 31341-31352, 2020.

S&P GLOBAL. The Sustainability Yearbook: Percebendo riscos, medindo o impacto e divulgando resultados – passos críticos para impulsionar a sustentabilidade corporativa no futuro 2020. Available in: www.spglobal.com/esg/csa/yearbook/files/SAM_TheSustainabilityYearbook2020_Portuguese.pdf

SILVA, V.H.F. Estudo e investigação do modelo de certificação B Corporation e sua relação com sistemas integrados ISO. Instituto Superior de Engenharia do Porto. 159p, 2021. Available in: https://recipp.ipp.pt/bitstream/10400.22/20124/1/DM_VitorSilva_2021_MEM.pdf

SOUZA, T.S.; FARIA, J.A. Demonstração do Valor Adicionado (DVA): uma análise da geração e distribuição de riquezas das empresas listadas no Índice de Sustentabilidade Empresarial (ISE) – B3. Revista de Gestão, Finanças e Contabilidade, v. 8 (2), p. 137-154, 2018.

SISTEMA B. Entenda seu impacto socioambiental. Plataforma Brasil, 2021. Available in: https://sistemab.org/br/brasil/

STREIT, J.A.C.; GUARNIERI, P.; FARIAS, J.S. Inovação no contexto da Logística Reversa e da Economia Circular: descobertas recentes e pesquisas futuras através do methodi ordinatio. Desafio Online, v. 10, n. 1, 2022.

THEIS, V.; SCHREIBER, D. Análise Reflexiva acerca das Contribuições da TI Verde para a Sustentabilidade Corporativa. Desenvolvimento em Questão, v. 19 (56), p. 264-281, 2021.

THEIS, V. Gestão de Resíduos Sólidos em empresas metalomecânicas de pequeno porte. Revista de Gestão Ambiental e Sustentabilidade, v. 7 (2), p. 230-247, 2008.

VILELA, B. A inovação a serviço da sustentabilidade: a experiência do Observatório de Inovação para Cidades Sustentáveis. Parcerias Estratégicas, v. 25 (50), p. 37-52, 2021.

WOOT, P.; KLEYMANN, B. Changing the cultural paradigm of management education: an imperative not an option, 11p. 2011. Available in: www.researchgate.net/publication/301629104_Changing_the_cultural_paradigm_of_management_education_an_imperative_not_an_option

YOSHIDA, C.Y.; VIANNA, M.D.B.; KISHI, S.A.S. Finanças sustentáveis: ESG, Compliance, gestão de riscos e ODS. Ed.: Abrampa, Belo Horizonte, 2021. Available in: www.mpf.mp.br/regiao3/atos-e-publicacoes/publicacoes/e-book-financas-sustentaveis-esg-compliance-gestao-de-riscos-e-ods-1

YUNUS, N.S.N.; RASHID, W.E.W.; ARIFFIN, N.M.; RASHID, N.M. Muslim’s Purchase Intention towards Non-Muslim’s Halal Packaged Food Manufacturer. Procedia-Social and Behavioral Sciences, v. 130, p. 145-154, 2014.

ZELDIN, S.; MCDANIEL, A.K.; TOPITZES, D.; CALVERT, M. Youth in decision-making: A study on the Impacts of Youth on Adults and Organizations, 68p., 2000. Available in: www.ojp.gov/ncjrs/virtual-library/abstracts/youth-decision-making-study-impacts-youth-adults-and-organizations